Alberta Carbon Market Reset

May 15th Canada-Alberta Implementation Agreement

May 26, 2026

On May 15, 2026, Canada and Alberta signed an Implementation Agreement formalizing commitments first outlined in the November 2025 Memorandum of Understanding (MOU), translating the MOU's commitments into tangible next steps. The agreement reaffirms the continuation of the Technology Innovation and Emissions Reduction Regulation (TIER) market and provides clarity on key market drivers out to 2040, with several changes that allow it to deviate materially from the federal backstop. This coincides with a commitment from Canada to advance approval of a new pipeline to the Pacific Coast, seeking designation as a project of national interest under the Building Canada Act. The pipeline is explicitly tied to the Pathways Project, a 16 Mtpa emissions reduction project anchored by at least 6 Mtpa of carbon capture.

The Agreement covers four broad areas:

- Core mechanics of the TIER regime, including benchmark stringency, future TIER Fund (“Headline”) prices, a post-2030 “Price Floor”, and limits to the Direct Investment Credits

- Reaffirmed commitment that Pathways and the oil pipeline project are “mutually dependent”

- Incentives for new abatement projects, including CfDs, CFR crediting, and EOR ITC eligibility

- Ongoing coordination on decarbonizing Alberta's power sector

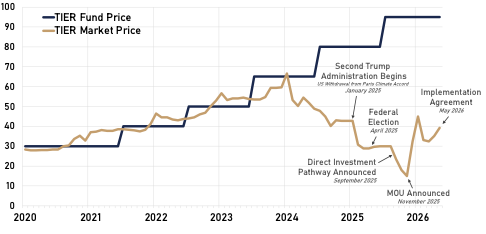

The Agreement comes after a tumultuous 18 months for the TIER market. Traded prices began to disconnect from the Fund Price, or “Headline Price”, in mid-2024 following a steady build-up of EPCs and offsets. A more dramatic price decline began in mid-2025, with prices falling as low as $17/t as uncertainty surrounding the future of the market intensified. In the week following the announcement of the Implementation Agreement, quoted offset prices rose from roughly $36/t to around $40/t.

Figure 1: Historical TIER Market Price vs. Fund Price

CAD per tonne CO2e, Monthly Average

The Implementation Agreement materially strengthens confidence in the future of Alberta's carbon market after a period of existential uncertainty. However, the Agreement clearly prioritizes industrial competitiveness and advancing specific decarbonization investments (i.e., the Pathways Project) over near-term TIER market tightening. Relatively lower stringency and the issuance of Direct Investment Credits are likely to prolong the time needed to draw down the existing bank of EPC and offsets, delaying convergence of traded credit prices with the Fund Price.

Changes to the Core TIER Mechanics

The Agreement introduces changes across four components of the TIER market: the stringency of Facility Specific Benchmarks (FSBs) and High-Performance Benchmarks (HPBs) across key sectors; the trajectory of the Fund Price; the introduction of a minimum transfer price for traded credits; and changes to the Direct Investment option.

Much of the discount observed in traded credit prices reflects the oversupply in the market and a growing credit bank, estimated at roughly 60 Mt to the end of 2025. Relatively reduced stringency and the continuation of the Direct Investment option, albeit at a lower rate of credit generation, mean the bank will draw down more slowly, keeping traded prices at a discount to the Fund Price for longer. This makes the Minimum Transfer Price, or Price Floor, an important market feature as the bank draws down through the early 2030s.

As explained in earlier notes (see “Alberta TIER 2024 Compliance Results: Implications for a growing EPC/Offset Bank”), the TIER Fund price will not “bind” as the marginal cost of compliance – and price of EPCs and Offsets – until the future year at which the bank has been drawn-down and TIER's maximum retirements (90% of obligations for 2026 onwards) consistently exceed EPC/Offset creation.

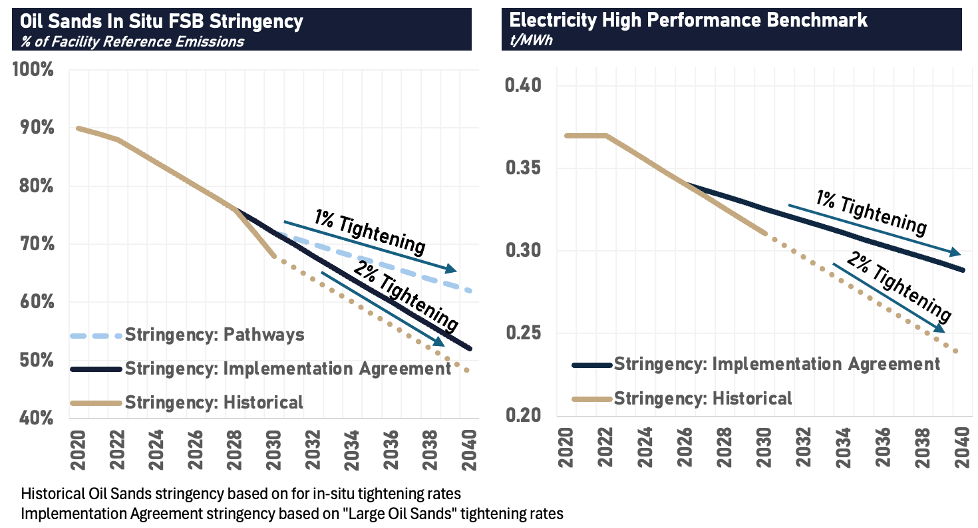

Stringency – Tightening Rates

The Agreement locks in sector-specific annual tightening rates for FSBs and HPBs through 2040, extending beyond the present benchmark standard which only specified stringencies to 2030. The tightening rates under the Implementation Agreement to 2030 are slower (i.e., comparatively less stringent benchmarks) relative to the prior stringencies. Oil sands stringency is now differentiated between “large” and “small” operators, with a higher rate applied to Pathways members should they fail to meet their Pathways commitments. “Large” and “small” oil sands operators are not defined in the Agreement; however, based on the production capacity across oil sands facilities, Foundation Economics interprets “large” oil sands operators as inclusive of all Pathways members.

Figure 2: Key Benchmark Stringency: Historical vs. Implementation Agreement

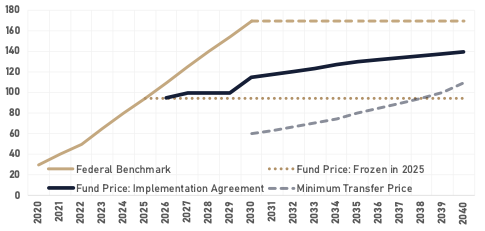

TIER Fund Price (Headline Price)

The Agreement replaces the frozen $95 Fund Price with a defined escalation path: $100 per tonne in 2027 through 2029, $115 in 2030, $130 in 2035, and $140 in 2040, with 1.5% annual inflation escalation from 2036 (see Figure 3). This is materially below the prior trajectory under the Federal Benchmark (set in 2021), which targeted $170 per tonne by 2030, landing roughly midway between that trajectory and the frozen $95 through the 2030s.

Minimum Transfer Price (Price Floor)

Alberta will enact a price floor regulation to take effect starting in 2030. The minimum transfer price will be $60 per tonne in 2030, rising to $110 by 2040 (see Figure 3). Importantly, the floor applies only to credits obtained and used to satisfy a TIER compliance obligation; any credit retired for compliance purposes must carry a value of no less than the floor price in the year of transfer or the year it was obtained.

Additionally, the Agreement indicates that credits generated prior to the enactment of the Price Floor (given Alberta’s intention of enacting this Price Floor by December 31, 2026, this presumably includes credits for 2026 and prior vintages) will be “grandfathered” and eligible for transfer below the Price Floor.

The amendments to the TIER Regulation that Alberta must introduce to implement the Price Floor will also need to address several unresolved specifics, including the treatment of forward sales and bundled credit transactions (e.g., power purchase agreements where the credits accrue to the purchaser).

It is worth noting, however, on a plain reading of the Agreement’s text, the Price Floor will apply narrowly to credits at the point of retirement for compliance (i.e., to satisfy emitters’ obligations), not to all credit transfers. Any credit retired to satisfy a TIER obligation must have been obtained at no less than the applicable floor price. However, on a strict reading of the Agreement, credits can still be held or transferred below the floor; they simply cannot be used for compliance unless acquired at or above it.

For credit creators, the Minimum Transfer Price may not guarantee they will receive the floor price. In a surplus market, liquidity from purchasers for compliance may be limited if they have sufficient inventory and no immediate need to purchase. That is, the imposition of the Price Floor may diminish liquidity in the secondary market and leave many credit creators reliant on purchasers who will transact below the floor (i.e., in speculative banking for future sales to emitters with compliance obligations against which to retire credits).

Figure 3: TIER Fund Price and Minimum Transfer Price

CAD per tonne CO2e

Direct Investment Credits

The Direct Investment option was enacted through an Order in Council on December 3, 2025, just days after the MOU was signed, with many critical details still pending, including eligible projects and issuance requirements. The Implementation Agreement preserves the option but constrains it, capping eligible investment amounts at 50% of capital costs net of ITC, ACCIP, and other government grants, and explicitly requiring Alberta to administer the program "in a manner that preserves market function and the Effective Price."

That commitment reflects a real risk. Unlike EPCs and offsets, investment credits are generated based on eligible capital expenditure, not verified emission reductions, representing a meaningful departure from the foundational principle of TIER. The Direct Investment option also creates a strong incentive for large emitters to structure capital programs strategically to maximize credit generation against their own compliance costs. The potential scale is significant: even at the new 50% cap and net of ITC, the capital expenditure associated with Pathways construction alone could generate a substantial volume of investment credits relative to current annual market volumes.

Two constraints limit the broader market impact of the Direct Investment option: investment credits are non-transferable and can only be used in years where an emitter has a compliance obligation. Importantly though, the present TIER Regulation (as amended in December 2025) does not limit the use of investment credits to a “regulated facility” but rather to the “person responsible for a regulated facility”, which would reasonably be read to allow a given facility’s legal owner to “pool” any investment credits for use across any obligations of its facilities. As well, the TIER Regulation allows for other credits (EPCs and Offsets) retired against obligations in the prior three years to be reactivated in exchange for investment credits. This feature allows for a certain amount of investment credits to be effectively transferable. Those planning large capital expenditures on decarbonization projects would be expected to strategically structure and time their outlays in consideration of these incentives.

Interlocking Commitments for TIER Market, Pathways, and Bitumen Pipeline

The Agreement reaffirms the commitment of Pathways members (Canadian Natural Resources, Cenovus Energy, ConocoPhillips, Imperial, and Suncor Energy) to deliver 16 Mtpa of emissions reductions. A minimum of 6 Mtpa of explicit CCUS is to be in-service by 2035, with the remaining 10 Mtpa not necessarily required to come from CCUS, and to be fully deployed by 2045. Importantly, the Agreement flags that a trilateral MOU with the Oil Sands Alliance for the Pathways Project remains to be agreed.

Nonetheless, the Agreement links approval of a future bitumen pipeline to the Pacific Coast (described in the MOU as capable of transporting at least one million barrels per day beyond the Trans Mountain expansion) to the Pathways abatement commitments, stating that construction of the two projects is "mutually dependent".

Given the timing of the Pathways projects (with full deployment not required to 2045), more details are necessary to understand how the success of these two projects will be linked in practice. Canada commits to pursuing designation of the pipeline as a project of national interest under the Building Canada Act. However, consistent with the MOU, any pipeline would need to be privately financed, and private sector financing remains to be secured.

More subtle is the link between the success of the Pathways Project and its outsized impact on TIER market balances. Successful Pathways projects will generate credits over their operating life, but the more immediate effect comes during construction. Capital-intensive CCUS projects will produce a significant volume of investment credits through the build phase, likely extending the timeline for drawdown of the credit bank well into the 2030s.

However, should a Pathways member fail to meet its commitments, it would face a significant effective penalty arising from the difference between the 1% annual FSB tightening rate applied over 2031–40 to firms building and operating the Pathways Project and the 2% annual tightening rate applied to “Large Oil Sands” operators. Such higher stringency penalty would materially increase obligations across that member's entire portfolio. Given the scale of the Pathways members' combined emissions, the resulting increase in market demand would be substantial and difficult to overstate.

New Incentives for Abatement Projects

In addition to confirming the extension of the Alberta Carbon Capture Incentive Program (ACCIP) and the Carbon Capture, Utilization, and Storage Investment Tax Credit (CCUS ITC) to 2035, the Agreement introduces several new incentives designed to support abatement project investment. These include jointly issued Carbon Contracts for Difference (CfDs), a confirmed minimum crediting rate for upstream CCUS projects under the Clean Fuel Regulations (CFR), and the extension of the Investment Tax Credit (ITC) to support enhanced oil recovery (EOR). While these incentives are directly relevant to the Pathways Project, they are not exclusive to it and will be available to other abatement projects across the province.

Contracts for Difference: An important new instrument in the Agreement is the jointly issued Carbon Contract for Difference (CfD). Canada and Alberta will co-fund CfDs covering up to 75 megatonnes of emissions reductions, on an equal cost-shared basis, with a maximum liability of $600 million per party. This implies total government exposure of $1.2 billion and would then translate to a $16 per tonne maximum exposure across the covered volume. The exact structure of these contracts remains to be confirmed; whether they function as true contracts for difference against a price index or as direct offtake agreements will determine how credit price risk is actually transferred and to whom.

CFR Stacking: The Agreement confirms a minimum 20% crediting rate for upstream CCUS projects under the Clean Fuel Regulations in all circumstances, a benefit unique to carbon capture in oil production and directly relevant to Pathways. Recent quotes for CFR credits have exceeded $400 per tonne (see our earlier note “Understanding Canada’s Other Carbon Price”). At such CFR credit prices, the 20% crediting rate would translate into $80 per tonne in additional revenue per tonne of CO2 captured. Given the TIER floor of $80 per tonne in 2035, this means that CFR revenue may be as valuable as TIER revenue for some CCS projects.

EOR Eligibility: Initially announced in the 2026 Spring Economic Update and reaffirmed in the Implementation Agreement, the ITC has been extended to EOR projects, a category not previously eligible. Projects tied to EOR will receive the ITC at half the standard rates, with an effective rate of 25% on eligible capture equipment through 2035. For carbon capture developers with EOR potential, the access to ITC opens a meaningful additional revenue stream that was previously unavailable.

Electricity: Further Direction to Come

Canada's National Electricity Strategy, released on May 14th, one day prior to this Agreement, provides clear context for the electricity commitments that follow. The Agreement echoes several of its core goals, including collaborative language around facilitating a doubling of Alberta's electricity grid by 2050, support for intra-provincial transmission as well as inter-provincial interties, and the establishment of a Canada-Alberta Electricity Working Group mandated to advance net-zero greenhouse gas emissions from the electricity sector by 2050. This is complemented with commitments to collaborate on future nuclear and AI strategies.

Importantly, the Agreement also confirms the continued abeyance of the Clean Electricity Regulations (CER), and a commitment to negotiate an equivalency agreement should the law be upheld following ongoing legal challenges. Also notable is Alberta's commitment to implement changes to the Restructured Energy Market (REM) to ensure continued investment in renewables.